Authors: Biniam Bedasso and Mohamed Abdiweli Ahmed

This post was originally published by the Center for Global Development.

The International Monetary Fund and World Bank Spring Meetings concluded with another round of “mission” announcements, underscoring the growing role of multilateral development banks (MDBs) as platforms for tackling problems that require scale, coordination, and sustained finance. This year, Water Forward was rolled out, aligning more than 10 MDBs and development finance institutions behind the goal of water security for a billion people by 2030. Last year, Mission 300 was launched and has a similar coordinated architecture, that aims to connect 300 million people in Sub-Saharan Africa to electricity by 2030. Both initiatives rest on the same premise: when MDBs align behind a shared target, they can help unlock action and financing that fragmented efforts cannot. They also do something less visible but equally important: they help set the policy agenda, signalling to client governments, donors, and technical agencies that a problem merits sustained political attention and institutional follow-through. So, why have school meals been left out?

School meals now present a similar question of coordination and scale. Governments are expanding their national programmes, and new global targets are emerging. Few investments promise to deliver benefits across multiple sectors—education, social protection, nutrition, and agriculture—the way school meals do. Beyond the cost-benefit metrics, school feeding addresses an overwhelming moral imperative. Today, millions of children go to school hungry, and millions more are out of school because of poverty. Expanding access to school meals could alleviate hunger that causes suffering and impedes learning, and create a powerful incentive to draw more children into school.

The political opening is there. At the Rio G20 Social Summit in November 2024, the Global Alliance Against Hunger and Poverty’s 2030 Sprint for School Meals brought governments, UN agencies, philanthropies, and two MDBs behind a goal of reaching 150 million more children in low-income countries (LICs) and lower-middle-income countries (LMICs) by 2030. Other commitments have followed. The School Meals Accelerator is working toward 100 million more children. The African Development Bank (AfDB) and Children’s Investment Fund Foundation (CIFF) have committed to reaching an additional 10 million children through the End School Age Hunger (ESAH) Fund. Taken together, these commitments signal genuine momentum, but they remain fragmented and fall short of the scale and coordination that a multi-MDB platform could help mobilize.

Set these numbers covered in the above commitments against the gap they are meant to close: around 745 million children are enrolled in primary education worldwide, yet only half are covered by publicly-funded school meal programmes. Of the roughly 379 million primary school children not reached, 266 million—or around 70 percent of the coverage gap—are concentrated in LICs and LMICs. So why have MDBs not aligned around a target for these children?

An MDB-aligned target would not close this gap on its own, but it could help concentrate finance and technical support in countries where domestic demand is growing fastest and fiscal space is weakest.Governments have already signalled demand. More than 100 countries have joined the School Meals Coalition, with 68 countries submitting national commitments. Worldwide, they spend $84 billion a year on school meal programmes. Across Africa, coverage grew by an additional 20 million children between 2022 and 2024. MDBs, by contrast, have not moved in lockstep. This does not mean they have ignored school meals, nor that they lack reasons for caution. But it does suggest a mismatch between rising country demand, the scale of the coverage gap, and the absence of a collective MDB offer comparable to those now emerging in water and energy.

What MDBs bring to the table

Engaging MDBs matters for three reasons. First, it can help mobilise resources for fiscally constrained countries. Second, and arguably more important, it fosters technical and policy leadership in international cooperation. Third, it can exercise agenda-setting power: when MDBs define an issue as a serious investment priority, they can reinforce the political and policy commitments of client governments rather than merely respond to it. As Chris Humphrey puts it, “No other kind of organization combines a public policy mandate, a multilateral cooperative framework, global expertise, and the financial firepower to make investments at scale.”

The MDB profile fits school meals better than is often assumed. School meals shouldn’t be viewed as just a recurrent expenditure. They are a multi-component system that includes kitchens, local procurement and supply chains, clean cooking, water and sanitation, and the digital systems that hold delivery together. Most of these components are exactly what MDBs are built to finance. The recurrent food cost (poorly suited to sovereign borrowing) can stay with governments. At the same time, the infrastructure and systems (including policy advice and technical assistance) around them are where MDB capital lands most naturally, particularly through concessional financing windows that offer grants and near-zero interest loans and MDB trust fund resources. Indeed, food costs constitute by far the largest share of the typical school meals budget, which could limit the potential contribution of system-level support to long-term sustainability. However, once the efficiency gains from system strengthening and capital investments are taken into account, it becomes clearer how MDB financing can complement government spending and support a more sustainable financing model.

Some MDBs have begun to step up: the AfDB with CIFF through the ESAH Fund, the Islamic Development Bank with the World Food Programme (WFP) through the Nutritious Start Initiative, and the Inter-American Development Bank with WFP through the Nutrition and Resilience Co-Financing Facility. Others, including the Asian Development Bank and the New Development Bank, are yet to develop comparable initiatives. The World Bank, however, is the most glaring absence in the adoption of a strategic approach to school meals. As the largest single source of development finance for LICs and LMICs, the World Bank invests only around $22 million a year in school meals, and unlike some of its peers, has no dedicated financing mechanism or partnerships to match.

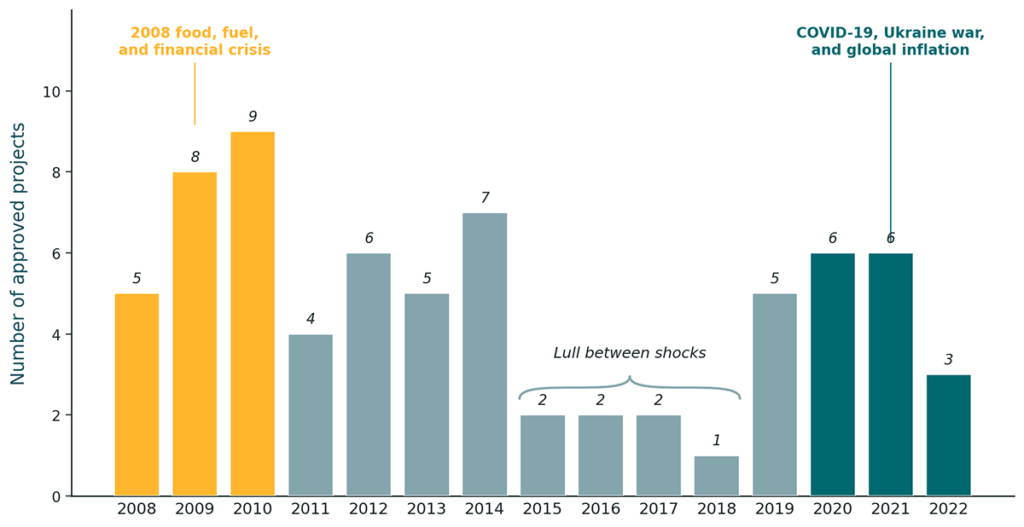

A closer look at the World Bank’s school meals portfolio reveals some instructive patterns. A recent review identified 71 projects supporting school meals across 36 countries between 2008 and June 2023, with a total operational volume of at least $282 million. The more telling finding is in the timing (Figure 1). Project approvals spiked in the years after the 2008 food, fuel, and financial crisis, slowed after food prices declined in 2015, and rose again from 2020 onward in response to COVID-19 and Ukraine-related inflation. Over one-third of all projects were classified as emergency or temporary responses, half were horizontal expansions of existing national programmes during a shock, and only a handful involved more than one Global Practice (the World Bank’s sectoral units, such as education, health, social protection, agriculture, and water).

Figure 1. World Bank school meals projects appear more shock-responsive than strategic

This pattern suggests that the World Bank may still consider school meals programmes a contingency instrument for use when shocks hit, rather than a standing line of engagement in human development. That framing matters: shock-response financing is, by design, short-term and absorbed into broader emergency packages—poorly suited to the multi-year systems-building on which durable national programs depend.

Siloed architecture, not a lack of evidence or country demand, is the real barrier

Before deploying financing, MDBs want to be confident on two fronts: that there is strong evidence of prospective impact and sustainability of the programme, and that there is country demand for it.

Take the evidence first. For school meals, it is strongest for attendance, enrolment, and food security; it is more mixed or sparse for learning, chronic malnutrition, and local agricultural multipliers. Costs also vary widely, and many countries still lack robust data on programme quality, unit costs, and implementation fidelity.

Now consider borrower demand. MDB loans must be repaid, and there are arguments suggesting that countries may decline to borrow from MDBs for social programmes such as school meals. The Bank’s school meals portfolio review points to the contrary: country demand to borrow has been real, with two-thirds of the projects financed through IBRD or IDA lending. Demand has also extended to IDA grants and World Bank-administered trust funds, which together account for nearly a quarter of the Bank’s portfolio. But it is also worth noting that, in the MDB context, supply can often create demand, given their agenda-setting role.

Both concerns are worth weighing. But the evidence gaps and country demand are unlikely to be as important as two deeper constraints: how the MDBs are structured and how each silo within them approaches school meals.

Start with the MDB architecture. Like the governments they serve, most MDBs are structured in silos—health, nutrition, agriculture, education, and so on—and school meals financing is all too often an orphan that has no divisional home. The World Bank’s recent human capital framing recognises that human capital is not built through sectors alone, but through coordinated investments across homes, neighbourhoods, workplaces, and multiple policy systems. This framing is directly relevant to school meals, which combine education, nutrition, social protection, agriculture, and local delivery functions. Yet the World Bank’s and other MDBs’ school meals portfolios appear to have been shaped more by operational entry points and sectoral mandates than by this integrated human capital logic. The result: school meals are often treated as a short-term shock response or sector-specific support rather than as a long-term, multi-sector human capital investment.

There is also the issue of how each sectoral practice views school meals. Education teams weigh them against interventions that deliver more learning per dollar. Social protection teams favour cash transfers. Nutrition teams cite strong evidence from the first 1,000 days on stunting and cognitive outcomes. Agriculture teams lean toward supply-side support. Each silo is responding to the needs of its sector, evaluating school meals against its own benchmarks or orthodoxies. None of those benchmarks captures the full cross-sectoral return of school meals, leading to flawed and undervalued assessments of the potential benefits of school meal programs. Alderman et al. (2025) made this point with hard numbers. Their evaluation of the Ghana School Feeding Programme valued its poverty-reducing effect alongside its long-run contribution to learning, finding that up to half of the value came from the poverty side alone. A standard education-focused benefit-cost analysis would not register that.

However, there are early signs of movement within some MDBs. Cross-sectoral approaches are being explored, and a few dedicated units are forming—most notably the AfDB’s ESAH Fund. The lesson from the World Bank portfolio is not that MDBs have done nothing. It is that engagement has been episodic, often crisis-linked, and not yet matched by a sustained institutional home or financing pathway.

What MDBs can do that governments and bilateral donors cannot

Why involve the MDBs at all? Governments are already scaling school meals through national budgets, and bilateral donors are providing gap-filling support across fragile and low-income contexts. What MDBs add is something different: long-term capital for delivery systems, policy and technical assistance, and countercyclical financing when shocks shrink fiscal space for school meals, and agenda-setting power that can help keep school meals on the policy table after the immediate crisis has passed.

Water Forward and Mission 300 are both missions whose outcomes are still to be determined. But each has done what the school meals space still lacks: each has aligned MDB incentives around a single target that two or more banks commit to help countries meet. These missions aim to meet existing country demand and, through their coordinated support, help create new demand over time. A school meals mission could do the same while leaving room for country choice over targeting, menus, procurement models, and the balance between domestic and external financing.

Whether school meals get an MDB-aligned target depends on how the banks collaborate, coordinate internally across sectoral portfolios, and allocate scarce concessional finance. Governments are not waiting for the MDBs. The question is whether MDBs can respond to that demand by leveraging their comparative advantages through instruments that support school meals as part of long-term, multi-sectoral human development policy. A school meals mission—modelled on Water Forward and Mission 300—would be a good place to start.

Photo: Children having a meal at school, Ghana; Arne Hoel/CC-BY-NC-ND 2.0